Air ambulances show why medical transport is really an operational discipline

Air ambulances sit in a unique corner of transport. They are fast, expensive, and often used when time matters most. That also makes them unforgiving. A recent air ambulance crash in eastern India, which killed seven people on board, is a hard reminder that medical transport is not only about clinical care. It is also about operational discipline.

The risk isn’t just in the air

In any medical transport mission, there are two jobs happening at once.

One is clinical: stabilise the patient and manage care during transit.

The other is operational: make sure the mission is safe to run, end to end.

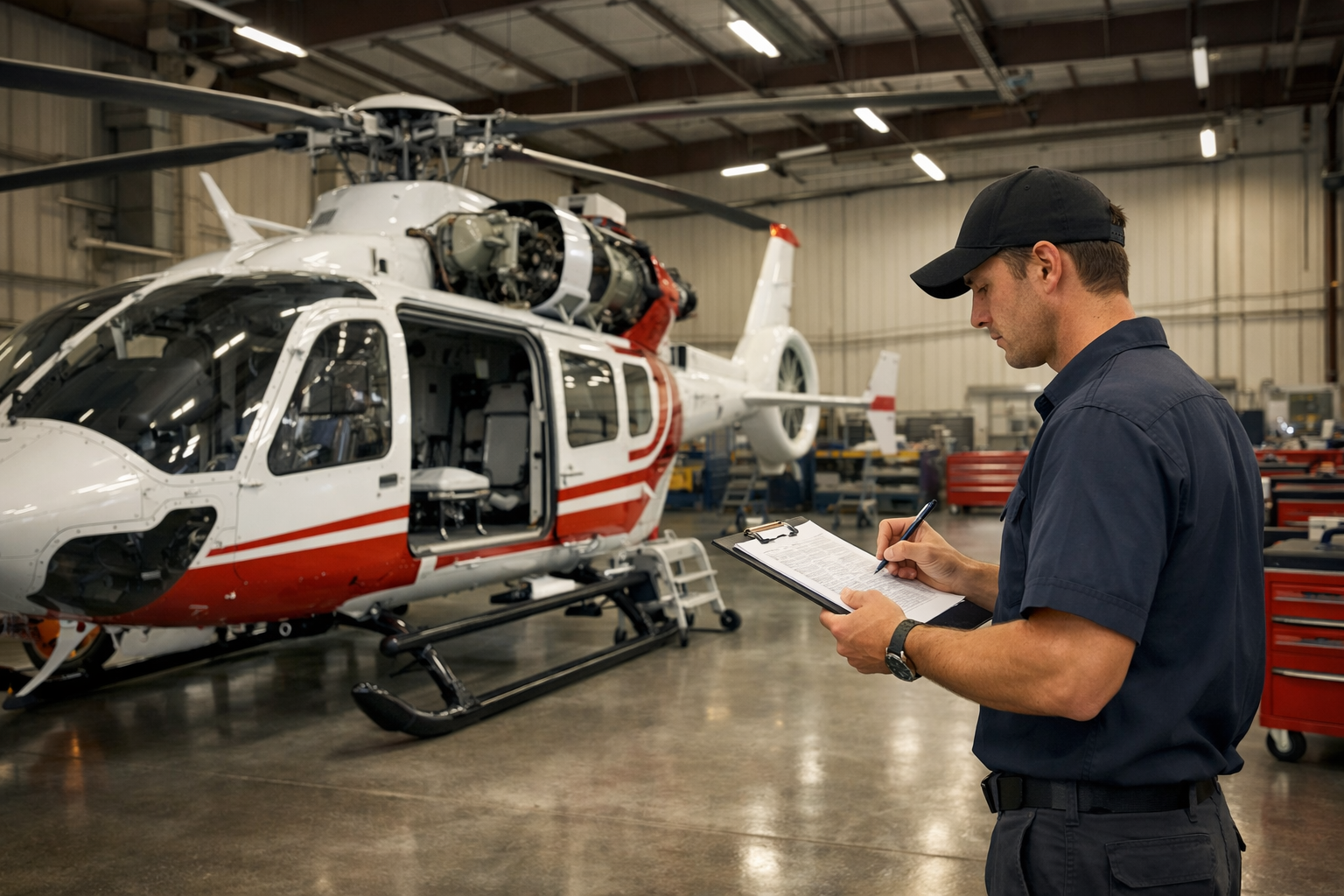

Operational risk covers the basics that can be easy to underestimate when urgency is high: weather, visibility, crew readiness, maintenance status, route planning, and coordination with receiving facilities. If any one of these is weak, the entire mission becomes fragile.

Why “go/no-go” culture matters

A lot of serious incidents share a similar pattern. Nobody sets out to take reckless decisions. What happens instead is subtle pressure:

a patient is critical

the family is desperate

the schedule is tight

an aircraft or crew is “available”

weather is “not ideal, but maybe manageable”

Over time, organisations can drift into treating risk as normal. That drift is dangerous. A strong operator builds a culture where “no” is an acceptable outcome, and where turning back or delaying is seen as professionalism, not failure.

That requires more than a policy manual. It takes training, clear thresholds, and leadership that does not reward risk-taking with praise or promotion.

What good operators do differently

In practical terms, safety-minded air ambulance operators tend to invest in the boring things:

consistent, documented pre-flight (or pre-departure) checks

robust maintenance planning and audit trails

crew rest rules that are actually followed

decision support tools for weather and routing

post-mission debriefs that capture near-misses, not just incidents

None of this makes headlines. But it reduces the chance of one bad day becoming a tragedy.

A message for funders and partners

If you finance, insure, or contract medical transport, you’re not buying “a flight” or “a vehicle.” You’re buying an operating system.

Safety systems affect reliability, downtime, claims, staff retention, and long-term reputation. In other words, they affect commercial viability. The operators who treat safety as a core operational asset, not a compliance exercise, are usually the ones who can scale responsibly.

Air ambulances are vital. They also demand a level of discipline that matches the stakes.

You might also like